Pension schemes are maturing, with a growing number nearing their endgame and closed to new members.

At the same time, The Pensions Regulator is in the process of revising the Defined Benefit funding code of practice, having completed the first of two consultations. The revised funding code proposes that schemes identify a long-term objective, specifying the funding basis and timeframe for reaching it.

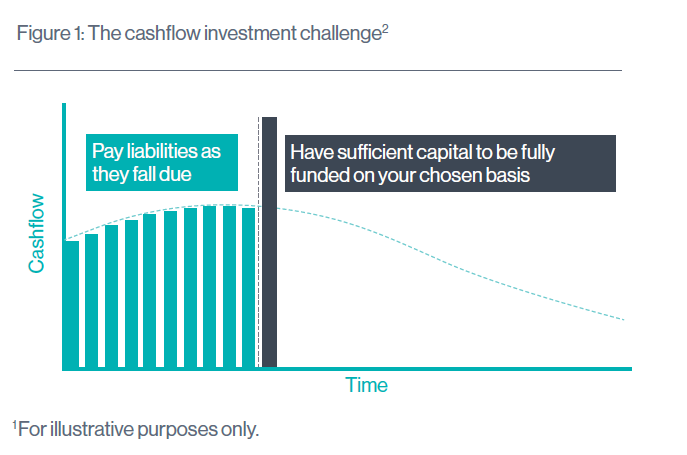

Pension schemes’ circumstances, and the regulator’s proposals, are encouraging pension schemes to set a long-term objective that results in a clearly definable cashflow funding challenge. We believe this has two features, in that pension schemes must:

1. pay the liabilities as they fall due on the journey towards the target time horizon, and

2. have enough capital to be fully funded on their target liability basis by their target time horizon.

This specification of the problem gives a clear and calculable ‘cashflow’ view of the funding challenge (see Figure 1).

Addressing the cashflow challenge

Even if the proposals for the revised funding code are changed as a result of the consultation process, we believe the focus on the investment challenge as a cashflow funding challenge will be appropriate for maturing pension schemes.

Rather than simply looking at current asset values and forecasting future expected returns, we believe a better approach is to structure a strategy that hedges liability risks, as many pension schemes do already through their liability-driven investment (LDI) strategies.

Having hedged these risks, the scheme can then focus on generating specific cashflows to sufficiently meet future cash requirements as they fall due, with a target of being fully funded at the end of the period. This would incorporate prudent assumptions for reinvestment risk, forced-selling risk and default risk.

For schemes targeting a high degree of certainty of success, we believe there are three unavoidable roles that assets will need to play:

1. Lock down the outcome: schemes will need to protect against the risk that the ‘gap’ between the value of their assets to their targeted cashflow outcome could widen. Assets can be used to hedge against scheme liability risks (such as interest rates, inflation and longevity) relative to the long-term objective. As mentioned above, most schemes already do this to some extent through their LDI strategies.

2. Manage cashflows: pension schemes will need to fulfil their cashflow obligations over the target time-horizon while progressing towards the long-term objective. This will mean considering how to meet cashflow requirements in order to minimise the risk of being forced to sell assets at inopportune times, while also generating returns to grow the assets. This is sometimes referred to as cashflow-driven investment, or CDI.

Constructing a portfolio of assets that generate contractually defined cashflows that broadly reflect a pension scheme’s required cashflows – either through income or maturing assets – can help pension scheme trustees strike this balance. High quality contractual assets, such as investment grade bonds, can help schemes generate a more certain return stream, avoid forced-selling risk and reduce dependency on the path of investment returns.

Where assets can be held to maturity, less liquid or more complex forms of credit can be used to generate additional income while still generating ‘natural’ liquidity.

3. Solve the problem: for schemes that are underfunded, a plan to grow assets through a combination of contributions and investment returns is also necessary – but generating those returns with the greatest certainty possible. For example, where it is possible to solve the problem using high quality bonds only, this would provide greater certainty than a solution involving a significant allocation to equities.

We believe an integrated approach that focuses on building a portfolio to deliver the outcome with the greatest level of certainty, monitored over time relative to the cashflow objective and with ongoing management to remove inefficiencies and manage risks, can help pension schemes achieve the security and resilience they are seeking on the path to the endgame.

Ultimately, we believe an integrated approach to the challenges trustees face will help them achieve their objectives with greater certainty, helping them to fulfil the pension promise and new regulatory requirements along the way.

Notes/Sources

This article was featured in Pensions Aspects magazine February 2021 edition.

Last update: 23 April 2021

You may also like: