Pension funds are in an unenviable position - trying to meet return targets of the past whilst managing liabilities against a backdrop of low yields, mounting inflationary risks and liquidity concerns. The hunt for yield may still be on but higher-yielding assets bring with them greater volatility.

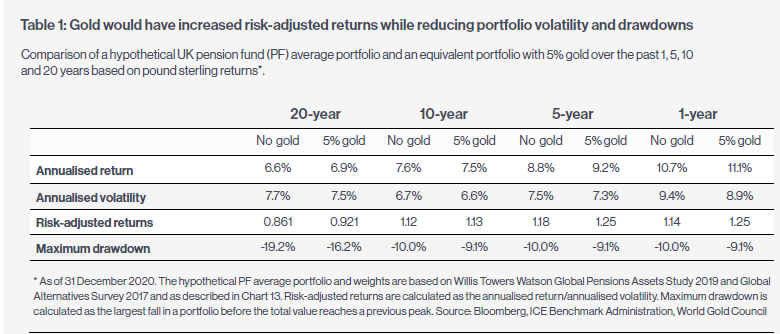

Consequently, effective portfolio diversifiers should therefore be a natural companion to riskier allocation strategies. And alternative assets are proving more popular amongst pension funds with this approach in mind. Gold is one of a handful of assets that can serve multiple and constructive roles in a portfolio and our analysis shows it is a clear complement to equities, bonds, and broad based portfolios. A store of wealth and a hedge against systemic risk and currency depreciation, gold has historically improved portfolios’ risk¹ adjusted returns (table 1) and provided liquidity to meet liabilities in times of market stress.

Gold is long recognised as a beneficial asset during periods of uncertainty. Historically, it has generated long-term positive returns in both good and bad economic times. Looking back almost half a century, the price of gold in US dollars¹ has increased by an average of nearly 11% per year since 1971 when the gold standard collapsed. Over this period, gold’s long-term return has been comparable to equities and higher than bonds.

We refer to gold as having a dual nature, and this is reflected by its diverse sources of demand and is one of the reasons why it differentiates itself from other investment assets. Gold is owned by investors to protect and enhance wealth over the long term as it is no one’s liability, and it operates as a means of exchange due to its global recognition. Gold is also in demand via the jewellery market, valued by consumers across the world, and it is a key component in electronics. Together, these diverse sources of demand give gold a particular resilience: the potential to deliver solid returns in various market conditions.

Gold market summary H1 2021

Gold’s behaviour during H1 not only highlighted its dual nature but also how its diverse sources of demand and supply interact. Gold was driven lower primarily by interest rates in Q1, and then again in late June, on the back of a more hawkish statement by the US Federal Reserve. Concerns of higher inflation offset part of the drag that interest rates brought. And the strong response from governments to aid the recovery through monetary and fiscal policies made some investors think about both currency risks and capital preservation. In addition, gold benefitted from a recovery in consumer demand in Q1, although second and third waves of the virus have presented challenges since.

Gold market outlook H2 2021

Looking forward, our analysis indicates that gold’s performance could continue to be heavily influenced by the movement of interest rates, the US dollar, and the economic recovery. For example, a further rise in interest rates could continue to create headwinds for gold. This is consistent with gold’s historical behaviour in periods when monetary policy becomes tighter, often resulting in price pullbacks.

However, we believe that central banks will be cautious in terms of the speed at which they start to remove asset purchase programmes or increase interest rates. A hasty move could result in large market swings and potentially destabilise the economic recovery.

Inflation is likely to remain a top of book concern. But while inflation has been on the rise in many regions, there are mixed views as to whether the increase in consumer prices will be temporary or more sustained. If price inflation becomes persistent, history shows that gold could perform well². Furthermore, gold appears more highly correlated to broader inflation metrics, such as growth in money supply, which could result in inflation bubbles, currency debasement, and potential market volatility around the world.

In summary, the short-term performance of gold is likely to be influenced by the direction of interest rates and the robustness of the economic recovery ahead. Yet for longer-term strategic investors such as pension funds, an allocation to gold could help boost overall portfolio health, and provide the resilience needed, as investors re-position for what promises to be a decisive decade ahead.

Notes/Sources

¹The relevance of gold as a strategic asset 2021 - US edition | World Gold Council

²Investment Update - Beyond CPI: Gold as a strategic inflation hedge | World Gold Council

This article was featured in Pensions Aspects magazine September edition.

Last update: 24 May 2024