Repos are widely used by pension schemes to increase their flexibility. They can generate additional cash to allow a scheme to target its growth objectives or meet near-term cash payments, while still ensuring liabilities are hedged.

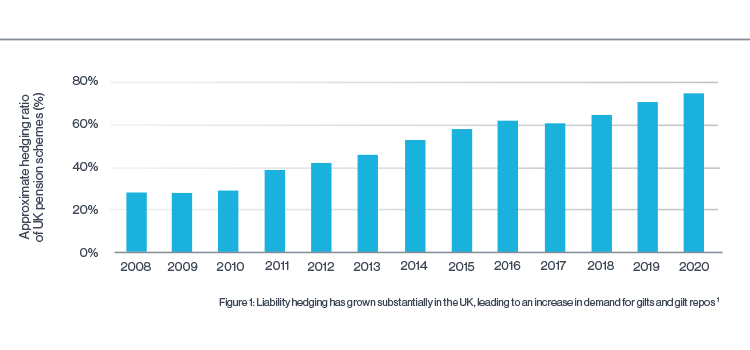

Their use has grown in parallel with the growth in liability hedging by UK pension schemes (see Figure 1), which has coincided with a shift towards using mostly gilts to hedge, rather than a blend of gilts and swaps.

For the most part, repo contracts have been conducted on a bilateral basis with banks as counterparties. However, bank-intermediated gilt repos have faced challenges, meaning alternative sources of repos are coming to the fore to help pension schemes maintain flexibility as they pursue their goals.

How bank-intermediated repos work

In a traditional repo, the pension scheme sells a gilt to a bank and agrees to buy back an equivalent gilt at a fixed price on an agreed date.

As the value of the underlying gilt changes over time, collateral payments are passed between the scheme and the bank daily. On the agreed date, the scheme receives back the gilt and pays the agreed cash value, plus an agreed interest cost (the ‘repo rate’). These repos are typically for less than 12 months and need to be replaced as they mature to maintain exposure.

Challenges faced by traditional bank-intermediated repos

Over the last decade, the growth in hedging, as well as regulatory and market developments, have driven material increases in demand.

The introduction of mandatory clearing of certain derivatives, and the trend for investors to sacrifice the ability to post gilts as collateral for bilateral swap contracts, have led to the potential for significant increases in demand for repos leading to a sharp rise in prices.

Market conditions in March 2020 were a stark illustration of this in action. The International Capital Market Association (ICMA) market report on repo market functioning during Covid-19 noted that “while the demand to access the repo market increased during the height of the crisis, banks’ capacity to intermediate that access did not. Buy-side participants report an increased reliance on the repo market as fund outflows drove the need to generate cash against holdings, as well as to meet margin calls against derivatives’ positions as volatility increased”2.

Bank regulations have also had an impact. Banks are required to hold capital against their repo book, making repos more costly for banks. This cost has been passed on to counterparties.

Such developments have led to UK pension schemes seeking access to other sources of gilt repos.

Additional sources of repos

To offer some examples, Insight has developed several alternative sources of repos for our UK pension scheme clients.

- Matching up the needs of UK pension schemes with those of money market investors: money market funds use repos to generate a return with high-quality securities as collateral. Building on this concept, Insight launched a strategy that pairs the cash of money-market investors with the repo needs of pension schemes.

- Cleared repos: Insight developed market infrastructure with RepoClear and other key partners to allow non-bank entities, including pension schemes, to access RepoClear, a market leading repo clearing service in Europe.

- Institutions, clearing houses and corporates: Insight has identified new types of counterparties, with appropriate credit quality, looking to manage cash balances in a secure and liquid way. Insight has established a panel of high-profile partners who undertake repo transactions with our clients.

In establishing significant new sources of repo liquidity, we have helped to maintain flexibility and generated substantial savings for our clients. We believe this means they are able to meet their objectives in a cost effective and low-risk way.

We also believe our efforts will support the wider industry, and encourage schemes to consider such alternative approaches, which have the potential to make a meaningful difference to their finances.

Notes/Sources

This article was featured in Pensions Aspects magazine November/December edition.

Important information - risk disclosures

Past performance is not indicative of future results. Investment in any strategy involves

a risk of loss which may partly be due to exchange rate fluctuations.

Portfolios which enter into repurchase and reverse repurchase agreements may be

exposed to losses if the counterparty does not fulfil its obligations to the portfolio.

This document is a financial promotion and is not investment advice. Unless otherwise

attributed the views and opinions expressed are those of Insight Investment

at the time of publication and are subject to change. This document is only directed

at investors resident in jurisdictions where our funds are registered. It is not an offer

or invitation to persons outside of those jurisdictions. Insight Investment reserves

the right to reject any applications from outside of such jurisdictions. Insight does

not provide tax or legal advice to its clients and all investors are strongly urged to seek

professional advice regarding any potential strategy or investment. Issued by Insight

Investment Funds Management Limited. Registered office 160 Queen Victoria Street,

London EC4V 4LA. Registered in England and Wales. Registered number 1835691.

Authorised and regulated by the Financial Conduct Authority. FCA Firm reference

number 122259.

© 2020 Insight Investment. All rights reserved. IC2442

1 Source: Insight Investment analysis, including historical data from KPMG and XPS LDI

surveys. As at 30 September 2020.

2 Page 5 of ‘The European repo market and the COVID-19 crisis: An ICMA European

Repo and Collateral Council (ERCC) market report’, published April 2020

Last update: 13 September 2022

You may also like: