The Pensions Regulator’s Climate Change Strategy – some key comments and next steps

The Strategy comments that TPR regards climate change as “systemically significant to pensions, to our regulatory regime and to our statutory objectives”.

As such, the importance of compliance with climate change requirements, both in respect of documentation and substantive steps, will understandably become a growing area of focus by the Regulator. This will be the case in both its educational and enforcement functions.

As regards compliance with the climate change requirements, Guy Opperman in an accompanying statement stated that “I applaud the commitment to update the Trustee Toolkit, and to properly enforce compliance with the basics”.

This approach is also mirrored in the Regulator’s Objective 1 in its Strategy that “we want to see schemes publish their SIP, Implementation Statement and, for those in scope, disclose their [Taskforce on Climate-related Financial Disclosures] TCFD report. Where they do not, and it is appropriate to do so, we will take enforcement action, which we may publicise”.

To recap on some of the key relevant SIP requirements, for schemes with at least 100 members, these are:

From October 2019 trustees have been required to adopt a policy on Environmental, Social and Governance (ESG) issues and include this in their Statement of Investment Principles. These requirements are divided into financial (including climate change) and non-financial material considerations (including ethics). This policy should be considered when making investment decisions.

From 1 October 2020: (i) Implementation Statements must be included in Annual Reports where a scheme’s Annual Report deadline is on or after 1 October 2020 (ii) From 1 October 2020 defined benefit (DB) schemes must publish their SIPs online (this requirement already existed for defined contribution (DC) and hybrid schemes) (iii) Trustees also need to include information in their SIPs on their policies regarding how asset managers’ performance and remuneration are reviewed in line with trustee policies. SIPs also need to include information on the duration of any arrangements with asset managers.

From 1 October 2021: Implementation Statements are required to be included in scheme SIPs and made available on a public website.

In addition, there are climate governance requirements for larger schemes. For schemes over £5bn, mandatory TCFD disclosure requirements will apply from 1 October 2021 (for schemes between £1bn and £5bn, it is 1 October 2022). Those schemes are required to report on TCFD by these respective dates or, if later, in their next audited accounts. These mandatory disclosures are in line with the task force’s recommendations. The TCFD provisions include a requirement for trustees to have oversight of climate-related risks and opportunities. Further, trustees will be asked to work out the scheme’s carbon footprint by calculating greenhouse gas emissions of the investment portfolio. Trustees will also have to set climate-related targets.

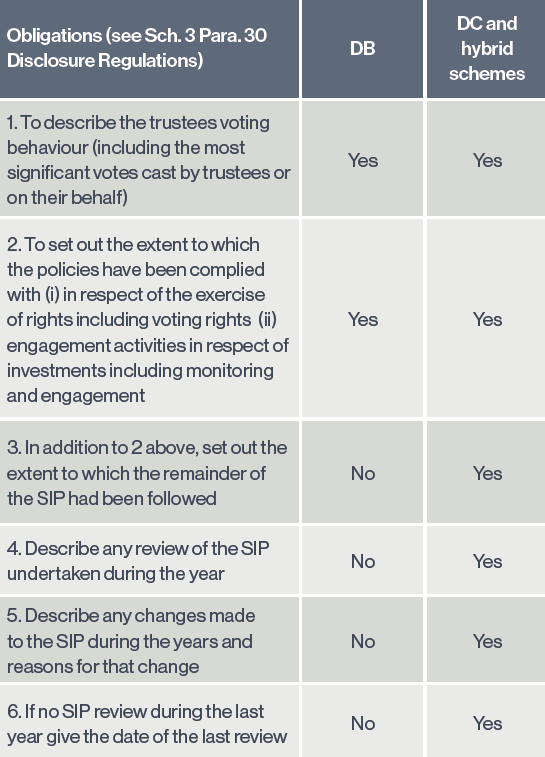

What needs to be included in an Implementation Statement?

The obligations of DB and DC schemes are summarised below in respect of Implementation Statements (See the Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013 as amended (The Disclosure Regulations). These include additional obligations for DC and hybrid schemes:

Items 2 and 3 above, in respect of following the requirements of the SIP, are required to be “in the opinion of the trustees” and, accordingly, it is important that the view expressed is that of the trustees rather than setting out or relying on the views of third parties.

Further commentary from TPR’s Strategy Statement TPR’s Strategy Statement also includes the following:

- TPR comments that stewardship activities help trustees monitor risk, and stewardship has a key role to play in ensuring that an investment portfolio is robust in the face of climate change

- TPR will review a selection of the Implementation Statements and publish our findings

- TPR encourages trustees to sign up to the 2020 UK Stewardship Code, which outlines best practice on improving investment governance and risk management; and on communicating activity and progress towards addressing systemic risks such as climate change

- Before the UN COP26 climate change conference in November 2021, TPR will publish a Climate Adaptation Report. This will include an outline of TPR’s plans towards using the recommendations of the TCFD, where applicable, as a framework for our own management of climate risk.

These comments reflect TPR dedicating significant resource to climate change issues including the active review of a selection of scheme SIPs. It will be important for trustees to engage with these SIP requirements and ensure that the SIP and Implementation Statements are considered fully and set out the position whilst paying heed to the specific circumstances of each scheme.

This approach reflects comments from David Fairs on 7 April that trustees: “should include devoting more board time to climate change, considering specific training, and, most importantly, integrating consideration of climate change right across decision-making”.

Further guidance is to come, and also additional detail in regulations, which mean that boards will need to keep an active and ongoing review of the requirements and recommended practice. In addition, TPR comments that a key policy driver is the government’s Green Finance Strategy that aims to transform the UK’s financial system for a greener future with new investment opportunities. One of the areas trustees may need to consider with care, and take advice on, is how to balance the climate change and other ESG requirements with the fiduciary duty to act in the best financial interests of members. This balance will need to take into account a wide range of factors including climate change issues and the relative return of ESG and non-ESG investments available to schemes, both in the short and longer term.

Notes/Sources

This article was featured in Pensions Aspects magazine June 2021 edition.

Last update: 1 August 2024