Confirmation of existing observation 2

Most UK pension schemes have already decided whether buy-out or self-sufficiency will be their endgame target

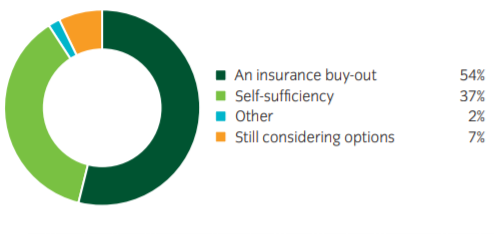

Over 90% of pension schemes responding to the survey have agreed their endgame target and are broadly equally divided between pursuing a buy-out or self-sufficiency (see Figure 1).

Figure 1: What is the target endgame for your defined benefit scheme? (Pick one)

Most UK schemes have an explicit target endgame date

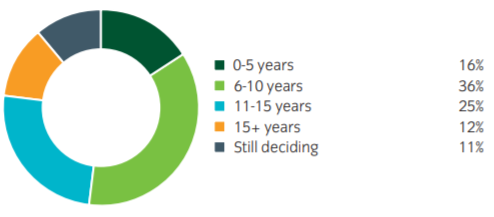

Only 11% of respondents do not have a finite endgame time horizon (see Figure 2).

Figure 2: What is the target time horizon for your endgame? (Pick one)

Figure 2: What is the target time horizon for your endgame? (Pick one)

Commentary from Insight Investment

UK defined-benefit schemes are generally in a strong position, with average solvency now close to levels prior to the financial crisis of 2008/2009. Combined with agreed additional future contributions, there is an opportunity now for schemes to secure all of their liabilities sooner than anticipated. However, as attention turns towards attaining specific outcome targets over ever-shortening timeframes, there is likely to be a greater need for outcome certainty. This may require a different investment approach.

New observations

A preference for de-risking evolution rather than buy-in or additional sponsor contributions

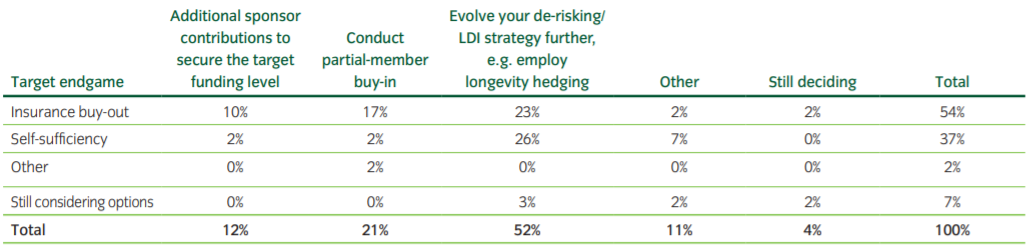

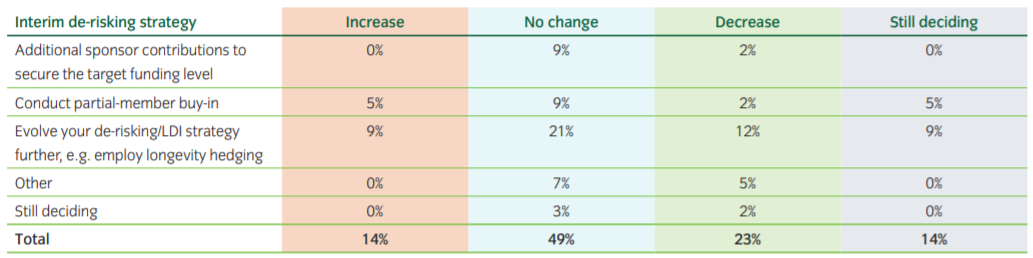

Most respondents have identified a clear route to reaching their goal, with the majority of respondents seeking to evolve their de-risking or Liability Driven Investment (LDI) strategies further as their primary tool on the journey to their target endgame. This option was more than twice as popular as any other option, such as partial buy-ins or seeking additional sponsor contributions (see Table 1). However, we acknowledge that respondents will utilise multiple de-risking strategies.

Table 1: What interim de-risking strategy are you most likely to employ on your journey to your target endgame? (Pick one)

"Focus on volatility. This becomes an increasingly material factor as schemes mature (i.e. less time to recover). Investment strategy needs to be aligned to funding strategy so that investments in assets of a contractual nature are increased as the funding position improves." - Trustee services manager, UK Master Trust

Commentary from Insight Investment

While 2019 has set another record for buy-ins and buy-outs, this has been dominated by a small number of very large transactions. The majority of schemes are looking to evolve their de-risking strategies – such as increasing liability hedges, introducing standalone longevity hedging and/or increasing their allocation to assets that provide ‘contractual’ returns – to help them get closer to their target positions.

Schemes are focusing on outcome certainty

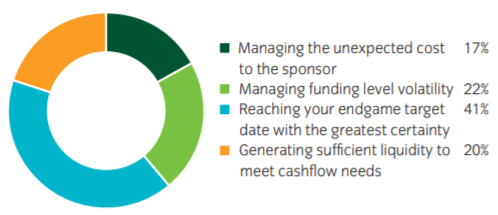

Most respondents to the survey said they would value further analysis on reaching their endgame target date with the greatest certainty.

Figure 3: Where would you benefit from further analysis when considering your endgame options? (Pick multiple)

"Assess the quantum of funding-level risks and determine possible responses now to be employed, if necessary, at a later date." - Chairman, UK pensions scheme, and director, corporate strategy

Commentary from Insight Investment

Ultimately, the key goal of any de-risking strategy is to narrow the range of potential future outcomes – meaning a scheme can be more certain of achieving its endgame target within its desired timeframe. Insight’s framework for helping schemes to evolve their strategy is based on three steps:

- Lock down target outcomes by hedging liability risks including interest rates, inflation and longevity

- Manage the uncertainty problem by investing in ‘contractual’ assets, such as bonds, to generate the returns needed to meet obligations

- Manage liquidity to ensure the scheme can cover its outflows and avoid being a forced seller in difficult markets

By adopting such an approach, we believe schemes can greatly increase the certainty of ultimately fulfilling their pension promise – and perhaps do so even sooner than they previously expected.

No solution can be 100% certain, so schemes should create buffers calibrated by stress testing any residual risks such as reinvestment risk or the risk of default in their bond portfolios. They should also construct portfolios that help to preserve flexibility to deal with setbacks.

The majority of respondents believe their next de-risking step will make it easier to attain their endgame – or at least, not make it more difficult

We gauge views on whether the next de-risking step will make it easier or harder for schemes to attain their endgame based on the impact of their strategy on the following three factors:

- required return on assets

- ability to hedge liabilities

- flexibility to deal with future uncertainty

For each factor, half of respondents believe that their chosen approach will have no impact on their ability to attain their chosen endgame (see Table 2 for the impact on required return on assets; read the full report for views on the impact on the other two factors). Of the remaining answers, respondents were much more likely to believe their approach would make it easier than harder to achieve this goal.

Table 2: How will your chosen interim de-risking strategy affect the required return from your remaining assets?

"Set a target and be flexible. Don’t buy-in too soon as you need the assets to generate returns." - Chair of trustees at a UK pensions scheme

Commentary from Insight Investment

Schemes should consider how their next de-risking step will impact their ability to reach their endgame target in the desired timeframe. One way that they can objectively measure this is by looking at the impact across the whole portfolio on the following factors:

- Required return on assets: Does the chosen de-risking step leave fewer assets to make up any funding level deficit? If so, this would increase the target return needed, everything else being equal. The pursuit of higher target returns increases the chance of defaults and negative returns.

- Ability to hedge liabilities: Does the chosen de-risking step divert assets away from hedging purposes? If so, schemes would either have to re-allocate funds for hedging purposes, potentially pushing up the required target return on non-collateral assets, or decide to accept a lower hedge ratio – either way, increasing risk.

- Flexibility: Up to the point of attaining the endgame target, there will always be risks affecting the assets or the liabilities that cannot be predicted or hedged. Examples could be poor short-term returns, transfer values forcing payments earlier than expected, or changes in legislation causing changes to benefits. Does the chosen de-risking step tie up a significant portion of assets which cannot be reversed? If so, this leaves the scheme with less flexibility to deal with any setbacks.

Notes/Sources

1 www.pensions-pmi.org.uk/about-us/pmi-insight-partners/de-risking-investment-strategies/

2 Examples include: Global Pension Risk Survey 2019, Aon, and European Asset Allocation Survey 2019, Mercer

RISK DISCLOSURES

Past performance is not indicative of future results. Investment in any strategy involves a risk of loss which may partly be due to exchange rate fluctuations.

Last update: 3 July 2024

You may also like: