Let’s imagine a world where people have quality pension provision, adequate savings and the necessary guidance and support to enjoy retirement. The next five years will see a significant shift in how pensions are provided and how people save for their later years. It’s expected Defined Contribution (DC) Master Trusts (MTs) will lead the way, playing a significant role in providing good value high quality pension schemes to millions of people, as well as support to their members and employers.

MTs are the favoured approach for employers to comply with their auto-enrolment (AE) responsibilities and as at October 2019[1]there were over 16 million MT members. This seismic change in where assets and members are, is altering the market, and in turn we will see a shift in the balance of purchasing power back and forth between providers, employers and members. More of that later.

The numbers

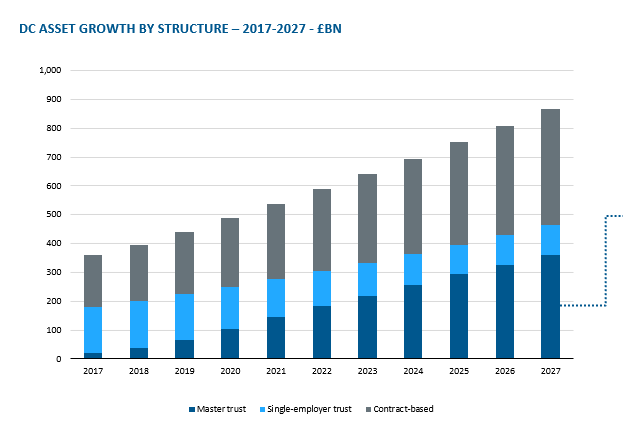

MTs are the fastest growing segment of the DC market, increasing from assets of £12 billion (2017) to £22 billion (2018), with membership numbers increasing by 43%. This exponential increase is largely driven by AE, and increasingly by single employer trusts consolidating into MTs. The rise in AE contributions in April 2019 led to further increases in MT assets. In addition, MTs with ‘in-scheme’ drawdown offerings will benefit from further growth.

By 2027, Broadridge estimates total UK DC market assets in accumulation will reach £867bn, with MTs accounting for £367bn of this[2]. It’s expected MTs will account for 78% of the trust-based market[3].

Market competition

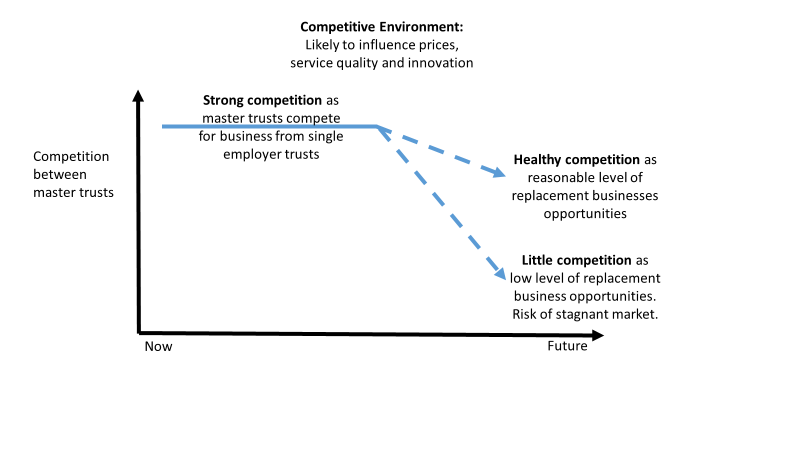

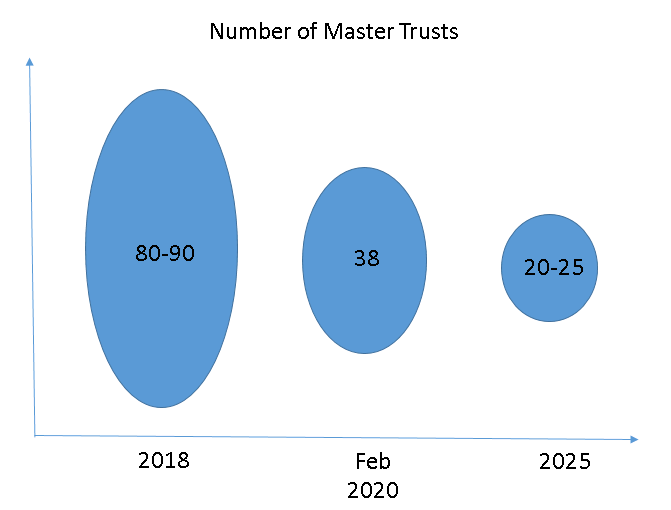

In the next five years we expect further market consolidation as commercial and regulatory pressures kick in. We believe the resulting number of MTs will reduce by 2025 - perhaps to between 20 and 25. These will be a mix of commercial, not for profit (AE models) and specialist MTs such as industry specific arrangements like the Railways Pension Scheme (RPS) or the Ensign Master Trust.

During this period, there will be intense rivalry between MTs, as the desire to reach scale will be key to longevity, financial sustainability and ultimately profitability for the commercial providers. In this period employers will be in the driving seat, with providers seeking to differentiate themselves through their brand, price, customer service, technology, guidance, their investment offering and retirement services amongst other things. Meanwhile most members will remain relatively passive recipients of the decisions made by their employer, often made with the help of their adviser.

As we come to the end of this five-year period, we expect there will be few, if any, new entrants

to the market. The barriers to entry due to stringent regulation, financial reserves, technology and administrative costs will be too high. We also expect the market for new employer clients from single-employer trusts to change as the flow of employers new to MTs will slow down. A secondary market will develop as some employers look to move MTs for better service and propositions to their employees. MTs will also win or acquire business from MTs looking to exit the market.

As the MTs chase business from employers unhappy with their existing MTs or looking to move their pension provision from a Group Personal Pension (GPP) to MT, a competitive and vibrant market may continue. There’s concern the costs and risks of change may appear prohibitive, but this may be overcome if the assets and cash flow are attractive enough to the provider to offer competitive rates. Growth will mainly be organic in terms of inflow of contributions and reliance upon their employer clients attracting new members, as opposed to single trust schemes being transitioned into MTs. MTs will become increasingly engaged with employers to work together to retain members and improve engagement to increase their contributions to secure improved retirement savings.

Continued Innovation

With fewer providers operating, will this stifle innovation? We believe not. The pensions savings world will see competition from other forms of savings products, not least the traditional GPP offering. Whilst it’s not yet clear how pension taxation will change, it seems certain there will be change in the future. Other savings products may become more attractive to savers (as opposed to members) if the attractive tax breaks attached to pensions are reduced. Pensions will still be attractive if members understand the benefit of their employer’s contribution. We will see more of a mixed economy approach to saving through various vehicles driven by the requirements of employers and savers. New products may be attractive due to flexibility, portability or as part of an employer’s well-being package. We will see MTs offering these vehicles alongside their traditional pensions offering.

Another driver for innovation will come from the members/savers themselves. The introduction of Pensions Dashboards will alert people to the opportunities available to them. They will see for the first time, their pension savings online, in one place. This has the potential to transform the pension and savings landscape. Individuals and advisers may consider moving assets so everything is in one place (or at least fewer places) or assets are invested based on each person’s specific circumstances, or just to lower costs. Pensions Dashboards should be a big benefit to people but it will shake up the market and there will undoubtedly be winners and losers. MTs could be amongst the winners but there are issues for them, in particular whether deferred members will switch to another MT or another savings vehicle. Will MTs compete to retain the deferred members’ pots whilst the new MTs encourage savers to transition?

As the Pensions Dashboards develop, we will see these substitute savings vehicles appear alongside pensions, providing a holistic view for members. We may see a time where members can easily switch their savings from one pension to another, or into a substitute vehicle at the click of a button. Although different tax regimes make this unlikely in the short term. MTs will need to keep innovating to prevent members and their savings leaving and consolidating elsewhere.

Summary

So, in five years’ time we expect to see 20-25 MTs in operation, continual innovation to meet the demands of employers and members, plus needing to retain members’ savings. The products will develop to be more holistic including options to save into other vehicles alongside the pensions arrangement. There will be a focus on legislation and the desire to introduce a greater degree of flexibility, similar to that enjoyed by retail savings providers. The regulatory focus on MTs will continue to be high and competition from the wider financial services market will be strong. Interesting times.

Notes/Sources

[2] UK defined contribution and retirement income, Broadridge Market intelligence report 2018

[3] Navigator 2018: UK defined contribution and retirement income, Broadridge

This article was featured in Pensions Aspects magazine July/August edition.

Last update: 23 April 2021

You may also like: