The genie is out of the bottle. Working life has changed, never to be the same again. It is surprising how quickly the phrase “new normal” has become a cliché, but that is exactly what is being experienced by people and companies in the pensions industry.

Remote and flexible working are not new concepts. Some organisations and individuals embraced these working practices before Covid-19. However, now that all and sundry have been forced to connect, collaborate, and cooperate digitally, the resilience of all employers, employees and customers in this new working environment has been tested. Whether the result is a pass, or a fail remains to be seen and will determine the permanency of any changes.

In the first of the Pensions Regulator’s statements on Covid-19, it said that it expected trustees to have appropriate monitoring and contingency planning in place and to be alive to risks that would have significant consequences for their scheme and members. The Pensions Regulator expects trustees to have a business continuity plan (BCP) and to understand their service providers’ business continuity arrangements. Sure, trustees need to think about what actions would be taken if certain events take place that would impact the running of their scheme. Yet, it is doubtful that before Covid-19 many schemes had BCPs that were drafted to cater for a complete shutdown of all offices everywhere.

Covid-19 and the ensuing lockdown required companies and trustees to move rapidly to virtual ways of working. There is a consensus that overall, the quick adoption of virtual working has gone reasonably well. Generally, trustees, executive teams and advisers have adapted quickly to remote working and online meetings. However, although the initial phase has evolved rapidly and there is a sense that things have calmed down into a more normative way of working, there are pitfalls. To be successful in the long term, a structured approach is needed, together with a significant investment to change corporate culture.

It has been shown that employees working for businesses in the pensions industry can work from home. A survey report by EY of more than 200 financial services firms saw 99% of respondents saytheir employees are working “productively and effectively”. Even the operations at the coal face, the administrators dealing with the members, have shown that administration teams can perform in this environment. Although, the ability to adapt is largely based on the capability of an organisation’s IT infrastructure and the technological prowess of its employees. From stories of daily team ‘pow wows’ to manage workflow and prioritise workloads, ‘elevenses’ networking events, team yoga classes, and even Friday night “quarantinis” (all via Zoom of course), some employees feel more connected with their teams and clients in a non-face to face world.

The initial switch to remote working caused by lockdown saw many employers and trustees scrambling to enact (and in some cases draft) BCPs, business continuity checklists, and flexible working plans to enable remote working and empower staff to work more flexibly. This forced the wholesale adoption and testing of technologies and ways of working that, due to various social and cultural barriers, have previously only existed in small pockets. That has changed. The contingency arrangements have been triggered and tested. The processes of trustees and employers have either been bolstered to cover a global pandemic or people are just muddling through, trying the best they can in the circumstances. In any case, the governance and documentation of pension schemes and employers should have been updated to include working practices that can be called upon if office working is not an option.

The coronavirus has accelerated the adoption of information technology. This is supported by the results of an EY poll on how the crisis will prompt changes across the financial services sector. Some 87% said that working from home during lockdown will prompt firms to adapt their technology faster than anticipated.

It is not just remote working that is here to stay. Many working practices have evolved in this environment, from meeting flexibility and focus, to the management of advisers. Most do not expect Covid-19 risks to retreat until Spring 2021, possibly not until 2022. Indeed, some sponsors are very risk averse on the return to offices. To be successful in this new normal state, the entire business needs to be operated virtually, for employees, suppliers, and other members of the ecosystem.

Aside from the web-connectivity challenge that this presents for some people, it also gives us a new set of challenges in terms of how we work. Now that the proximity factor has been taken away, all of us have had to think about how we are going to connect, collaborate and cooperate effectively. The outbreak will create long-lasting changes to the way we live and work. The pandemic will have a sweeping effect on every aspect of our lives, and it is likely that many of the changes we are making at this moment will become permanent.

Now that companies recognize that employees can relatively easily work from home, executives are likely to encourage this behaviour. As the benefits of remote work have become apparent our employment landscape has shifted for the long term and working from home may become the new accepted norm.

Yet there are still challenges. We are still in crisis mode and some potential issues are getting overlooked as everyone is focussing on the urgent stuff. There are bound to be questions and even legal challenges around data protection, employment rights, to what extent employers are responsible for people in their own homes, to name but a few. Some employers will retreat, others will push the boundaries as is always the case. Managers have had to learn to lose direct control. No more management by looking over someone’s shoulder. No more presenteeism in the office. This has been replaced by a virtual presenteeism, driven by redundancy and workload worries. It is harder in this environment for younger, less experienced people to grow in their roles. This may have an impact for trustee-related services broadly and on how boards can become more diverse.

By and large trustees have dealt with the current circumstances well; some becoming quite tech-savvy in the process. However, as time passes, some of the less immediately obvious challenges start to appear so it is helpful to think about how the trustee chair and the other trustees can continue to make effective decisions. Some trustee meetings have become more frequent, focussed, shorter, and strategic, whilst others have simply recreated their old practices over marathon video conference calls. Committees, sub-groups, and executive teams have come even more to the fore to get work done and socialise issues. This has added to workloads. In preparing for shorter, focused meetings, excellent adviser management is critical. Greater participation is encouraged when meeting virtually and the key role that the chair plays in that process is more defined, but more difficult. Selecting advisers and selecting new trustees remotely is doable, but it is not ideal. Similarly, inducting new trustees requires more attention and offline contact. The good behaviours and practices that have become even more important in lockdown should not get forgotten when measures ease in a non Covid-19 world.

One thing that will have changed at board level for most will be the realisation that scenario planning is needed to cater for uncertainty. No longer is it just about planning, efficiency and mitigating risk. Indeed, planning often mitigates against dealing with uncertainty as it does not allow for any slack. Simply, no one knows what will happen, where it will happen and when it will happen. The biggest outcome of Covid-19 will be a greater understanding of what uncertainty means.

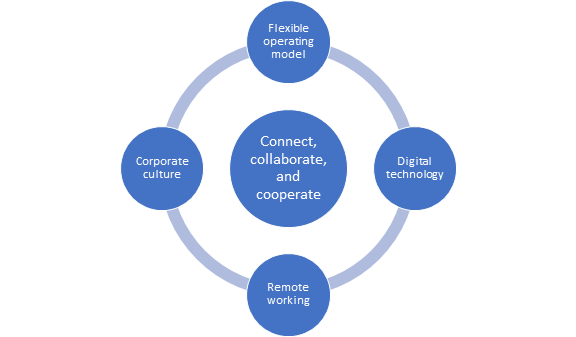

It is possible to break down the investments and benefits of unlocking and mastering this new paradigm into its component parts, like in Figure 1. Experience has shown that people and companies in the pensions industry investing in more flexible operating models and corporate culture that embrace remote working and digital technologies can deliver more effective connections, collaboration, and cooperation.

Figure 1: Investments and benefits of flexible remote working

Responding to Covid-19 has seen many people and companies realise that it had more to offer them than they had realised. Those that have embraced the technology, flexibility and new ways of working will welcome this new normal and consequently improve their success in dealing with it and the even newer world to come post lockdown. It will be hard to bring everyone back from home now they have tasted freedom from the shackles of a commute and the tyranny of open plan offices, sitting in a cubicle for eight hours each day. Eventually, we will overcome the coronavirus and go back to some sort of normalcy. Yet, certain pre-Covid-19 standards, such as flying around the world to meet clients, will be questioned as there is a lot more focus on the “S” in ESG. The winners out of all this will be those that have followed the unofficial slogan among the Marines to: “Improvise, adapt, overcome”, made popular by Clint Eastwood in the film Heartbreak Ridge and featured in memes starring Bear Grylls. For some, remote working and meetings may be the way things stay, particularly for the regular trustee meeting dates, but with strategy and training dates potentially returning to a face-to-face format. Others anticipate a mix of a phased return to office working in parallel with remote working, with both face-to-face and remote attendance at meetings once Covid-19 risks recede sufficiently. This may be a more workable solution to accommodate the preferences of members, employees, employers, and trustees as lockdown eases more generally.

Notes/Sources

[1] Eva Verbeemen and Sébastien Bujwid D'Amico, ‘Why remote working will be the new normal, even after COVID-19’, EY, Belgium, 9 April 2020, https://www.ey.com/en_be/covid-19/why-remote-working-will-be-the-new-normal-even-after-covid-19 (accessed 3 June 2020)

[2] Angharad Carrick, ‘Financial services firms unlikely to return to the 'old normal'’, City AM, https://www.cityam.com/exclusive-financial-services-firms-unlikely-to-return-to-the-old-normal-says-ey/ (accessed 3 June 2020)

[4]Eva Verbeemen and Sébastien Bujwid D'Amico of EY (n 1)

[5] The Economist – Briefing, ‘Less globalisation, more tech – The changes covid-19 is forcing on to business’, The Economist, UK, 11 April 2020, https://www.economist.com/briefing/2020/04/11/the-changes-covid-19-is-forcing-on-to-business (accessed 3 June 2020)

[6] The Economist – Briefing, ‘Less globalisation, more tech – The changes covid-19 is forcing on to business’, The Economist, UK, 11 April 2020, https://www.economist.com/briefing/2020/04/11/the-changes-covid-19-is-forcing-on-to-business (accessed 3 June 2020)

Bibliography

Angharad Carrick, ‘Financial services firms unlikely to return to the 'old normal'’, City AM, https://www.cityam.com/exclusive-financial-services-firms-unlikely-to-return-to-the-old-normal-says-ey/

Barry Mack, ‘Don’t let the urgent crowd out the important – Are you still making good decisions?’, Muse, https://www.museadvisory.com/site-login/resources/2020-05-18-musing-urgent-and-important-decision-making-v1-0.pdf

Eva Verbeemen and Sébastien Bujwid D'Amico, ‘Why remote working will be the new normal, even after COVID-19’, EY, Belgium, 9 April 2020, https://www.ey.com/en_be/covid-19/why-remote-working-will-be-the-new-normal-even-after-covid-19

The Economist – Briefing, ‘Less globalisation, more tech – The changes covid-19 is forcing on to business’, The Economist, UK, 11 April 2020, https://www.economist.com/briefing/2020/04/11/the-changes-covid-19-is-forcing-on-to-business

The Pensions Regulator, ‘COVID-19 (coronavirus): what you need to consider’, The Pensions Regulator, UK, 2020, https://www.thepensionsregulator.gov.uk/en/covid-19-coronavirus-what-you-need-to-consider

Last update: 20 December 2023

You may also like: